This is my last

mortgage

rate note before we reset the calendar. It seems like just yesterday that we entered last January with high hopes for more rate relief.

What we saw was industry-leading pricing tumbling:

- 50 basis points on popular three-year fixed terms;

- 30 basis points for the venerable five-year fixed;

- 85 basis points for variable mortgages.

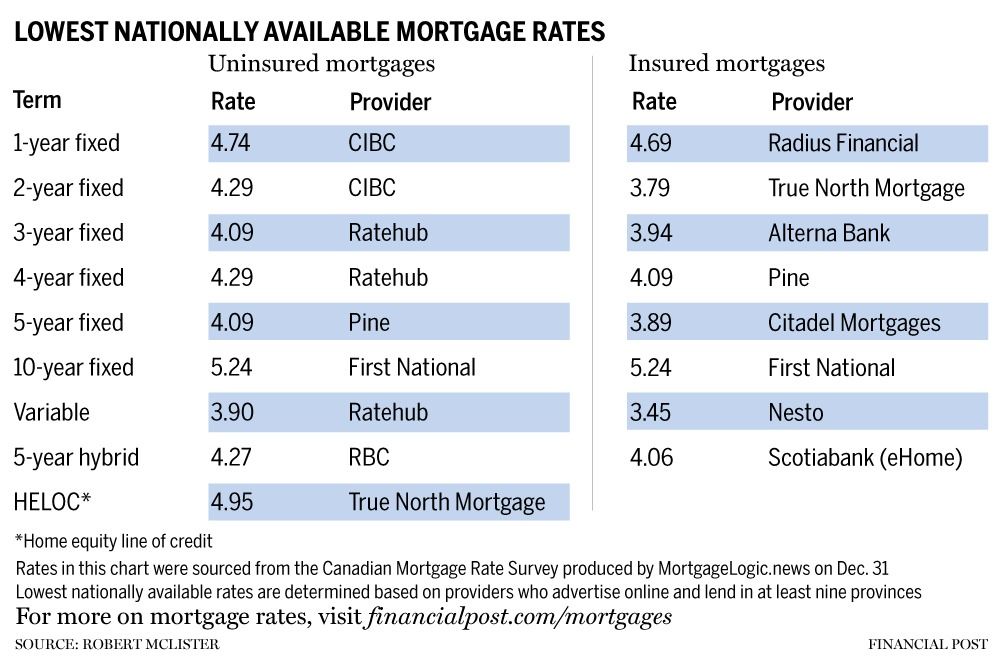

Every little bit counts, and despite the run-up in bond yields lately, a few default-insured rates still begin with a three. For example, look to national leaders such as:

- Nesto Inc.’s five-year variable at 3.45 per cent;

- Citadel Mortgages’ 3.89 per cent five-year fixed;

- Alterna Bank’s 3.94 per cent three-year fixed;

- True North Mortgage Inc.’s 3.79 per cent two-year fixed.

Well-qualified uninsured borrowers will pay the usual 10-to-30-basis-point premium for the privilege of not having to purchase default insurance.

Not to be outdone, regional players have even bigger discounts in some cases, including:

- B.C.’s Coast Capital Savings Credit Union with its 3.84 per cent uninsured three-year fixed;

- Coast Capital’s 3.94 per cent uninsured five-year fixed;

- Ontario’s Ratebuzz with a 3.69 per cent insured five-year fixed;

- Ratebuzz’s 3.39 per cent insured five-year variable;

- Butler Mortgage Inc.’s 3.64 per cent insured three-year fixed;

- Manitoba’s Access Credit Union Ltd.’s 3.45 per cent uninsured five-year variable.

As for the prime rate, it remains parked in a long-term holding pattern, and the next

Bank of Canada

meeting on Jan. 28 likely won’t change that.

Robert McLister is a mortgage strategist, interest rate analyst and editor of MortgageLogic.news. You can follow him on X at @RobMcLister.

This table reflects the prevailing rates at the time this story was published. For the best mortgage rates in Canada right now, click

here

.